27.11.2025 - 28.11.2025 | Berlin

EStALI Conference

We are delighted to announce this years EStALI Autumn Conference on European State Aid Law, which will be part of Lexxion’s 25th anniversary jubilee events in Berlin (November 26 – 28). We will discuss recent judgements of the European Courts,

Subscribe to our newsletter for updates on legal developments, upcoming conferences, workshops, and publications in your areas of interest.

Newsletter: Subscribe now

In the Spotlight

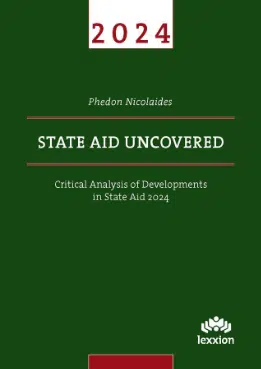

State Aid Uncovered

Critical Analysis of Developments in State Aid 2024

Author: Phedon Nicolaides

State Aid Uncovered presents analysis of the main policy and legal developments in the field of State aid in 2024 which was the first full year of the application of the new de minimis regulation (Regulation 2023/2831).

Lexxion is an independent publisher, conference organiser and training provider in Berlin, specialising in recycling and chemicals law in Germany, EU competition law, data protection law and structural funds at European level. The family-owned company offers specialist journals, conferences, workshops and book series. Through a network of renowned experts and co-operation with European and national authorities as well as academic institutions, Lexxion provides high-quality content and contributes to the culture of discussion and networking in Europe.

Current events

All events

State Aid: A Thorough Overview from A to Z

Applying State Aid Rules to Research, Development, and Innovation Projects

Anti-Fraud Game: Port Authority

State Aid Compliance for Services of General Economic Interest (SGEI)

Simplified Cost Options for HOME Funds

Summer Course: Financial Management of ESI Funds

Summer Master Class – “State Aid Uncovered” with Prof. Dr. Phedon Nicolaides

Summer Course: State Aid – Core Concepts, Principles, Exemptions, and Guidelines

EStALI Seminar – Strategic Autonomy and State Aid for Digital Technology

Chemikalienrecht außerhalb der EU

State Aid for Climate Action, Environmental Protection, and Energy Efficiency

Challenges and Expectations for the Post-2027 EU Funding Period

Praxis-Seminar: Biozidrecht

State Aid in the Transport Sector: Policies and Implementation

Indicators, Monitoring and Evaluation of EU Funds

Master Class: Public Procurement for Utilities and Concessions Contracts

AI and Public Procurement

Anti-Fraud Game: History and Modernity

Auditing EU Funds: Conflict of Interest and Transparency Issues

Winter Masterclass “State Aid Uncovered” with Prof. Dr. Phedon Nicolaides

EStALI Workshop

EStALI Conference

Berliner Abfallrechtstage 2025

19th European Food and Feed Law Conference

Simplified Cost Options for EU Funds

State Aid: A Thorough Overview from A to Z

Applying State Aid Rules to Research, Development, and Innovation Projects

Anti-Fraud Game: Port Authority

State Aid Compliance for Services of General Economic Interest (SGEI)

Simplified Cost Options for HOME Funds

Editorial News

All JournalsEHPL 1/2025 Out Now

The first issue of the European Health & Pharmaceutical Law Review (EHPL) for 2025 is […]

ICRL 2/2024 Out Now

Issue 2/2024 of the International Chemical Regulatory and Law Review is out now! This issue […]

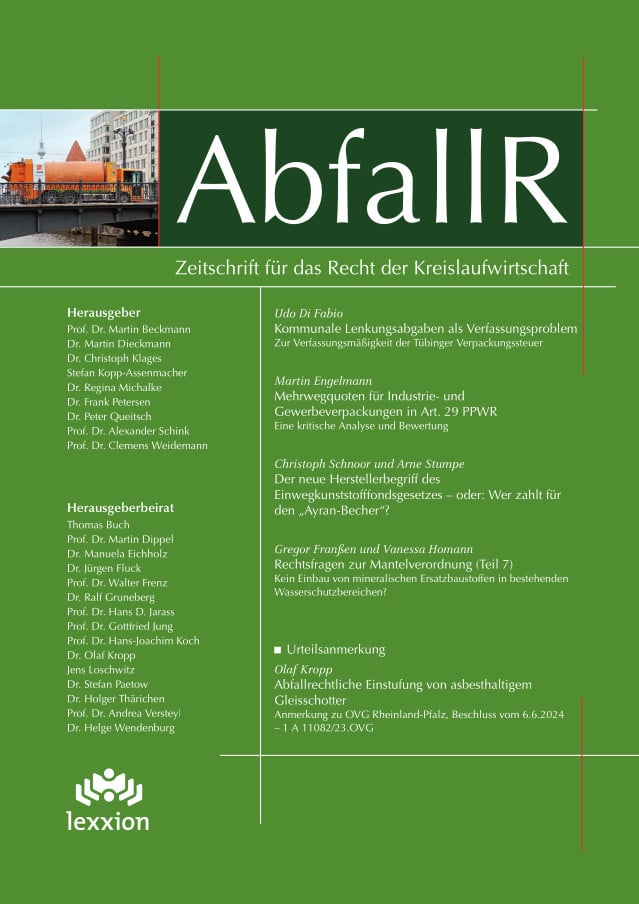

AbfallR 3/2025 jetzt verfügbar

Eröffnet wird die neue Ausgabe der AbfallR durch den Beitrag von Lemperle/Gruppe zur Novelle der […]

EFFL 3/2025 Out Now

Issue 3/2025 of the European Food and Feed Law Review is now available online! This […]

EDPL 1/2025 – Celebrating 10 Years...

The special anniversary Issue 1/2025 of the European Data Protection Law Review (EDPL) is out […]

EPPPL 1/2025 Out Now

Issue 1/2025 of the European Procurement & Public Private Partnership Law Review (EPPPL) is now […]

CoRe 1/2025 Out Now

Issue 1 of the European Competition and Regulatory Law Review – CoRe is now online! […]

UWP 1/2025 jetzt verfügbar

Die neue Ausgabe der UWP widmet sich einer ganzen Bandbreite aktueller umweltrechtlicher Themen und beantwortet […]

AIRe 1/2025 – The Growing Complexity...

Issue 1/2025 of the Journal of AI Law and Regulation (AIRe) is now available. The […]

CCLR 1/2025 Out Now

Issue 1/2025 of the Carbon and Climate Law Review is out now. The issue features […]

StoffR 1/2025 jetzt verfügbar

Aus aktuellem Anlass befassen sich die Beiträge im ersten Heft des Jahres vor allem mit […]

EStAL 1/2025 Out Now

Issue 1 of EStAL 2025 is now available online! Read the Editorial by Caroline Buts: […]

EurUP 1/2025 jetzt verfügbar

Was ist eigentlich unter „Umweltrecht“ bzw. „Umweltrechtswissenschaft“ zu verstehen? Ehmann/Sereda-Weidner eröffnen den neuen EurUP-Jahrgang mit […]

EHPL 1/2025 Out Now

The first issue of the European Health & Pharmaceutical Law Review (EHPL) for 2025 is […]

ICRL 2/2024 Out Now

Issue 2/2024 of the International Chemical Regulatory and Law Review is out now! This issue […]

AbfallR 3/2025 jetzt verfügbar

Eröffnet wird die neue Ausgabe der AbfallR durch den Beitrag von Lemperle/Gruppe zur Novelle der […]

EFFL 3/2025 Out Now

Issue 3/2025 of the European Food and Feed Law Review is now available online! This […]

Latest Blog Posts

All BlogsData Protection Insider, Issue 132

-CJEU: National Courts Authorising Personal Data Disclosure Are Not Data Controllers- On 30th April, the […]

Restructuring Aid

Introduction Following a formal investigation, the Commission in decision 2025/775 approved restructuring aid to TAROM, […]

How to Calculate the Amount of...

Introduction Public funding that offsets costs incurred as a result of compliance with legal obligations […]

Data Protection Insider, Issue 134

-ECtHR Reiterates That Police Processing of Personal Data Has to Follow Strict Conditions for Legality- […]

When Does Existing Aid Become New...

Introduction New State aid schemes have to be notified to the Commission for prior authorisation. […]

Competitors of Recipients of State Aid...

Introduction Perhaps paradoxically, a public authority can adopt a measure that confers an advantage to […]

Data Protection Insider, Issue 133

-CJEU Rules on Status of EDPB Opinion on Consent or Pay- On 29th April, the […]

The Italian Competition Authority investigates on...

On 26 March 2025 the Italian Competition Authority (“AGCM”) announced to have launched an investigation […]

Calculation of the Funding Gap of...

Introduction The European Commission recently approved a modification of a Czech scheme for the support […]

Tax Exemption of General Application

Introduction In November 2014, the General Court in case T-219/10, Autogrill v Commission, held that […]

Data Protection Insider, Issue 132

-CJEU: National Courts Authorising Personal Data Disclosure Are Not Data Controllers- On 30th April, the […]

Restructuring Aid

Introduction Following a formal investigation, the Commission in decision 2025/775 approved restructuring aid to TAROM, […]

How to Calculate the Amount of...

Introduction Public funding that offsets costs incurred as a result of compliance with legal obligations […]

Data Protection Insider, Issue 134

-ECtHR Reiterates That Police Processing of Personal Data Has to Follow Strict Conditions for Legality- […]